Following an acquisition, integration is no cakewalk. It is, in fact, much harder than signing the deal.

Unless you are a frequent acquirer, and have (successfully) completed a number of integrations, there is a high probability of being unsuccessful in realizing your strategic and financial acquisition goals: 50-70% of failed acquisitions (depending on who you ask) speak for themselves.

If you want to win a 10.000 meter-race, the keys to success lie in practice and creating the right conditions to excel. The same applies to acquisition and post-merger integration: A coach, training and repetition of the exercise increase the likelihood of a win tremendously.

If you are planning an acquisition, and view inorganic growth as an integral part of your strategy, internal capabilities will warrant a prosperous and rewarding program implementation. I will work with your M&A team to develop the right post-merger integration approach, and will train your team for future projects:

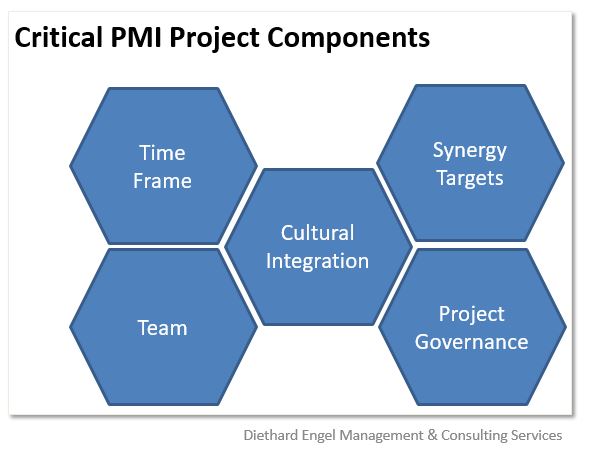

- Development of the target operating model

- Building and leading a strong team

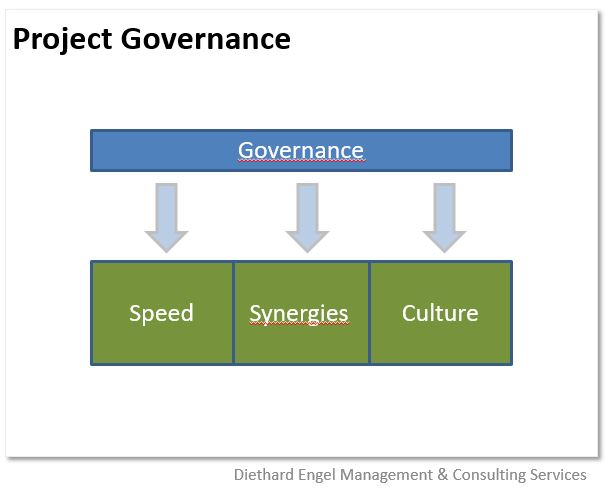

- Implement project governance and transparency

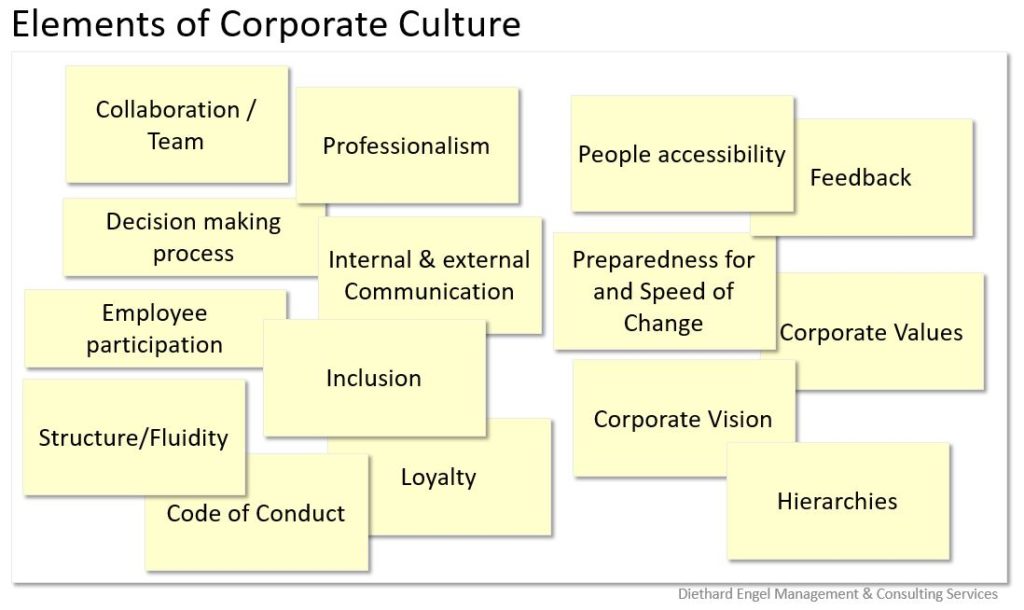

- Drive cultural fit

- Advise on internal and external communication

- Identify the right KPIs for Controlling

- Manage the timeline

Even if your project seems off track already, it is not too late to fix it: Doing nothing is usually not the best option.

I have successfully completed multiple PMI projects and can help you to get to the finish-line, too.

Based out of Germany, Diethard Engel is an independent consultant and interim manager, focused on Business Transformation, Post-merger Integration / Carve-out and Executive Finance. He has run multiple post-merger integration/carve-out projects for international businesses.